Who Shorted The War?

Two oil trades. Two Trump Iran pivots. One question regulators cannot leave unanswered.

The traders are still unnamed. That is exactly why the public deserves the answer.

“The public does not need a theory. The public needs the name.”

The full report is below — also published on Beehiiv — with its receipt trail and source ladder. Every claim below clears at two-of-three independent sources before publication, with right-of-reply offered to every named subject.

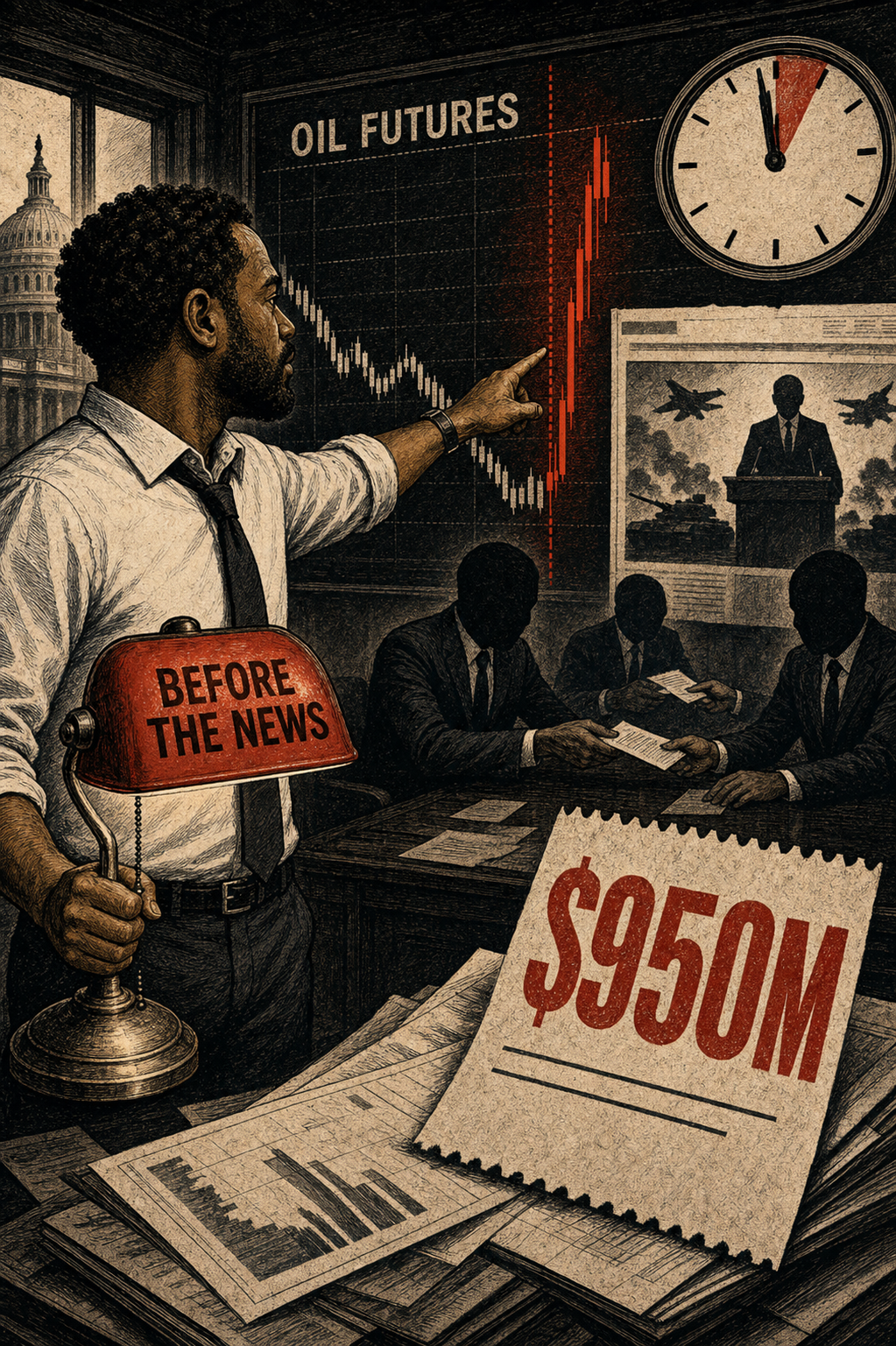

I have watched Washington pretend timing is a coincidence when timing is the whole story.

The vote before the donation. The contract before the announcement. The stock sale before the bad news. The trade before the war headline.

Power loves a foggy clock. If nobody can see the minute hand, everybody gets to call the pattern complicated.

So let us keep this simple. Before one Trump Iran announcement, traders reportedly placed more than $500 million in oil futures bets. Before another, Reuters reported roughly $950 million in bets on falling oil prices. Rep. Ritchie Torres asked the SEC and CFTC to investigate. The traders are still unnamed.

Somebody bet before the war news broke. The public still does not know who.

The Machine

Markets do not wait for moral clarity. They move on information.

That is why timing matters. Not because every well-timed trade is illegal. Not because every trader with a good guess committed a crime. Not because a headline alone proves insider trading.

It does not.

The clean claim is narrower and stronger. When enormous trades land minutes or hours before presidential war-policy announcements, the public deserves to know whether those trades were luck, analysis, market hedging, leaked information, or something worse.

That is not conspiracy. That is market integrity.

The Receipts

- The March trade. Reuters reported that traders placed 5,100 Brent and WTI crude futures lots, worth well over $500 million, about fifteen minutes before Trump delayed strikes on Iranian energy infrastructure. John Cassidy asked the public question plainly in The New Yorker.

- The April 8 referral. Torres publicly asked SEC Chair Paul Atkins and CFTC Chair Michael Selig to investigate suspicious oil and equity futures trading before the Trump Iran announcement.

- The April trade. Reuters later reported roughly $950 million in bets on falling oil prices a couple of hours before Trump announced a two-week ceasefire with Iran.

- The April 14 referral. Torres sent another letter calling for a joint SEC/CFTC investigation into the $950 million trade.

- The regulator posture. Bloomberg reported that the CFTC had sought exchange data, and S&P Global reported that CFTC Chair Michael Selig told lawmakers the agency would pursue fraud, manipulation, or insider trading.

That is enough for a question. Not enough for a conviction. Enough for a question.

The Translation

Do not let anyone move the goalposts.

The question is not whether BTP can name the traders today. We cannot. The question is not whether the public record proves insider trading today. It does not.

The question is whether the government can allow war-sensitive market moves to remain a mystery when the reported trades were this large and this close to presidential announcements.

That question answers itself.

Because if the answer is “we do not know,” then the next sentence has to be “find out.”

Who placed the trades? Were they hedges, institutional positions, or directional bets? Were the same accounts involved more than once? Did anyone have access to nonpublic information? Did any government official, adviser, family member, donor, contractor, foreign actor, or connected fund benefit?

If the answer is no, say no with evidence. But do not ask the public to watch a $950 million trade land before war news and accept vibes as oversight.

Read The Receipts Before The Spin

- John Cassidy, The New Yorker on the March timing problem.

- Reuters via GMA on the first trade.

- Rep. Ritchie Torres on April 8 and again on April 14.

- S&P Global on the regulator posture.

The Verdict

War power already gives presidents too much room to move markets with a sentence. That is why the market around the sentence matters.

If the trades were innocent, the public should know. If the trades were sophisticated hedges, the public should know. If the trades were placed by people with no connection to anyone inside the decision chain, the public should know. And if the trades were not innocent, the public should know that too.

The worst answer is the usual Washington answer: a fog machine, a committee letter, a regulator sentence, and then silence.

The public does not need a theory. The public needs the name.

This one is built to forward.

Drop your email and the next receipt lands where you can actually use it.

Receipts in this issue

Already on the list? Send this to one person who reads the fine print.

New here? Subscribe from this issue so the dashboard can count the public funnel, not just imports.